On Monday, Apple announced a handful of new subscription services, the most anticipated of which was Apple TV+. Specifics about the service are limited, though the high-production promo reels in the demonstration were many. Bottom line, Apple wants to be more than a hardware company—it wants to be a fully fledged service suite, and content is part of that strategy.

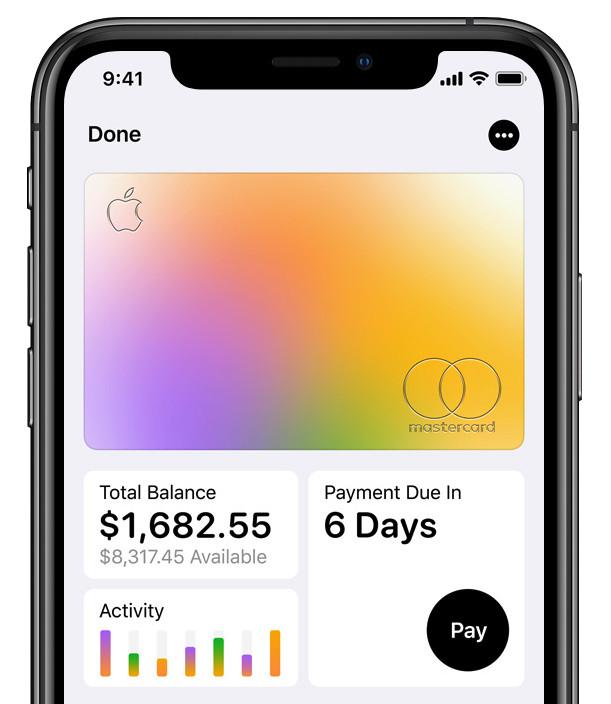

Another part of that strategy, as the world learned Monday, is consumer finances. Apple announced Apple Card, a “new kind of credit card” backed by Goldman Sachs that integrates with Apple Pay to offer a digital-first financing option for consumers. The card, which launches this summer, lives on the iPhone inside Apple Wallet; it also has a physical component, but users don’t need it so long as a business accepts Apple Pay. The physical card itself is fancy, a nod to consumer interest in cards that are heavy and/or sleek. The Apple Card is titanium, has no numbers or signature box, and features chip technology so owners can use it at non–Apple Pay businesses. However, Apple incentivizes owners to use Apple Card digitally with Apple Pay, and not the physical card; Apple Pay purchases yield a higher cash-back rate than those made with the physical card.

As with other financial apps, the convenience factor has its pros and cons. Users can sign up for an Apple Card directly on their iPhones and start using the digital option immediately upon approval. The ease with which iPhone users can acquire a new line of credit is concerning. It’s not difficult to imagine someone applying for an Apple Card in a few taps, being denied, and then dealing with a hard credit check that dings their score. Apple also gathers user data to make financial recommendations and provide users with information about their economic habits.

In other ways, the Apple Card is like a traditional credit card; once approved, owners will have to navigate the fine print. The card has a wide annual percentage rate (APR) range of 13.34 to 24.24 percent. Average-to-decent credit-score owners will get an APR somewhere in the middle: a standard rate, nothing special. The card offers 2 percent back on purchases and, predictably, 3 percent back on Apple purchases.

Apple is not the only technology company to venture into the financial market. In 2018, Google launched Google Pay—or rather, it combined its fragmented Google Wallet and Android Pay systems into one service. Samsung similarly has a digital wallet app called (no surprise) Samsung Pay. And while Facebook doesn’t have a mobile wallet, it began offering payment support in 2015. Users can opt to send and receive money using Facebook Messenger as an alternative to apps like Zelle and Venmo.

Perhaps the service that most closely resembles Apple Card is Google Store Financing. The little-mentioned payment option is specific to Pixel products and supported by Synchrony Bank, formerly owned by GE. Google Store Financing gives customers credit toward the purchase of a Pixel phone (or a purchase that includes a Pixel phone) from the Google Store; there is 0 percent APR on Google Store for the first two years, although that APR skyrockets to 29.99 percent if no phone is purchased. Like the average store- or brand-specific credit card, GSF has a low credit limit and high interest rates, and is handled by a bank that doesn’t have a brick-and-mortar presence. (For what it’s worth, Synchrony doesn’t have an amazing NerdWallet customer rating, though its services sounds fairly standard and it is FDIC-insured.)

But credit financing options and digital wallets don’t totally contain a consumer’s financial life the way the Apple Card potentially could. Cash-back rewards are paid out to users via Apple Pay, meaning users may be more likely to use Apple Pay over Venmo or Zelle for peer-to-peer transactions. With penalties incurred for transferring a balance to a debit card, it’s easiest and most beneficial for Apple Card owners to leave their money locked-in with Apple—plus there’s extra incentive to use Apple Pay and spend on Apple products. In most ways, the Apple Card is like any credit card: The majority of people will probably get an average interest rate and the rewards are aggressively fine. What makes it stand out are its limitations: It’s for iOS users only and it exists primarily to further bind buyers to the Apple ecosystem. That is, of course, what all digital platforms want to do—to be the machine operating every possible function of consumers’ lives. What better way to get there than to control their money?