The NFL’s Real Spencer Strasmore Is the Anti-‘Ballers’

After retiring from football in 2010, All-Pro defensive end Patrick Kerney began a second career as a financial adviser. But forget about yachts and fancy suits. For Kerney, counseling players and coaches is all about #KnowYourDough.The NFL’s Real Spencer Strasmore Is the Anti-‘Ballers’

After retiring from football in 2010, All-Pro defensive end Patrick Kerney began a second career as a financial adviser. But forget about yachts and fancy suits. For Kerney, counseling players and coaches is all about #KnowYourDough.

In April, Lisa Kerney, a SportsCenter anchor, sent a tweet to her husband Patrick, a former top NFL defensive end, about their 5-year-old son. “We may need to review the whole ‘investing’ idea again,” she wrote, attaching a photo of their kid’s homemade piggy bank: a Ziplock bag containing a tiny fistful of spare change and labeled “GUMBALL MONEY ONLY.” Patrick’s response was part proud parent, part personal-finance wonk, and entirely him.

“That’s my kiddo!” he crowed, then turned serious: “Short-term liabilities must have highly liquid assets allocated to meet them.” He ended with a hashtag that frequently appears on his Twitter feed and would also make a great name for a Wall Street bakery: “#KnowYourDough.”

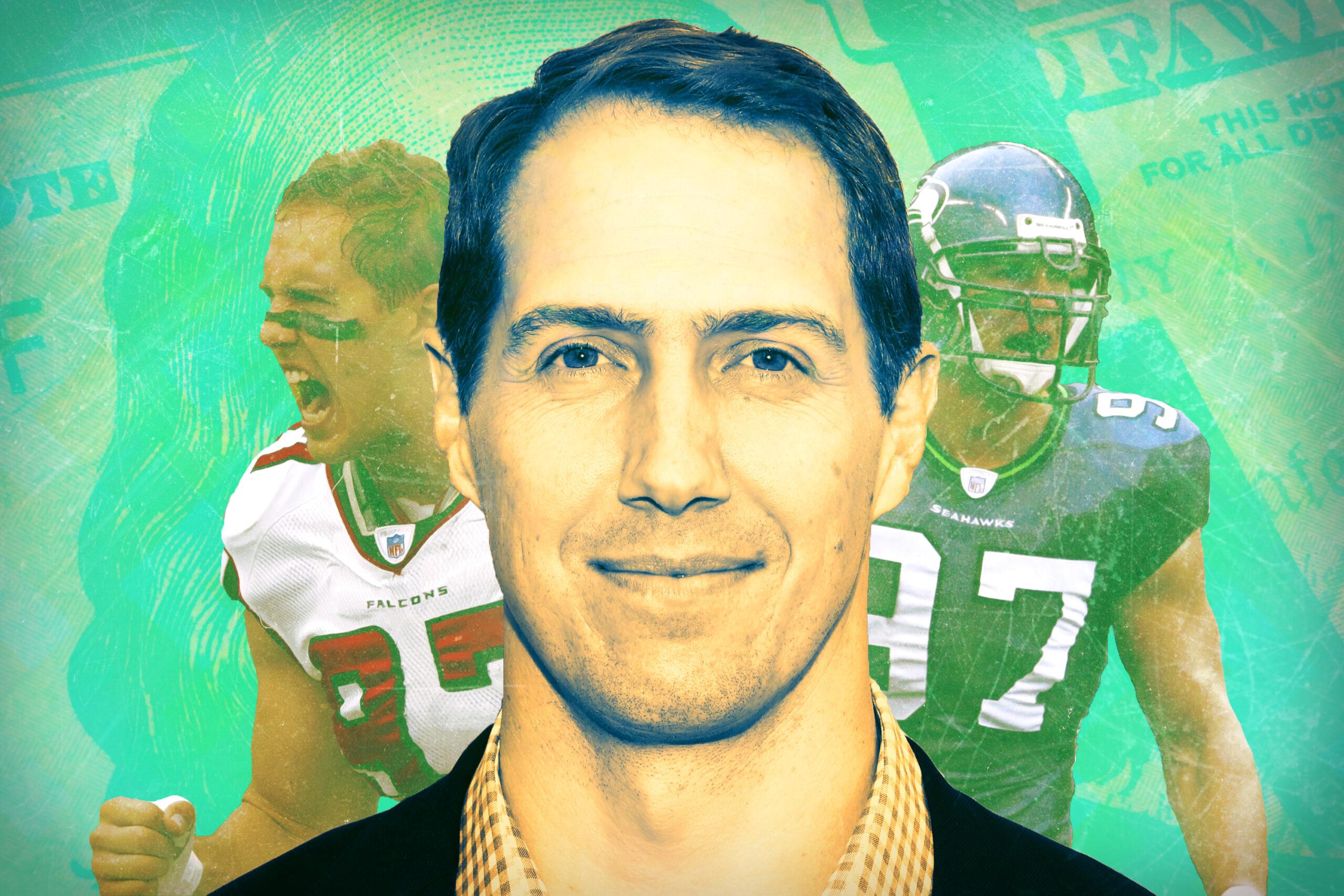

In his 11-season NFL career with the Atlanta Falcons and the Seattle Seahawks, Kerney came to know plenty about dough. He signed lucrative contracts—an $8.5 million signing bonus with the Falcons here; $19.5 million in guaranteed money from the Seahawks there—and delivered standout play: two Pro Bowl appearances and two All-Pro nods, and an NFC-leading 14.5 sacks in 2007. But if his name and personal wealth were built on his ability to take NFL players down, the reputation he has established since retiring in 2010 has been based instead on his commitment to lifting them up.

Around the professional sports world, stories about people who made millions but are now bankrupt appear with grim regularity. A perfect storm of large, lumpy cash flows, short career timelines, financial unfamiliarity, youthful vanity, constant peer pressure, and even altruistic ambition can lead to athletes overspending; getting burned by risky, unsuccessful investments; or even being straight-up swindled in fraudulent schemes.

“Part of my passion,” says Kerney, speaking by phone on a recent afternoon, “is like, when people who are in their early 20s are getting ripped off, it’s heartbreaking because a lot of these guys have overcome so much to get where they are already.” And so he has made it his mission to educate players (as well as his children, apparently) about how to best preserve and grow the earnings they’ve worked so hard to amass. In 2009, before his final season with the Seahawks, Kerney took part in a special several-day NFL-sponsored program at the Wharton School that prompted him to start seriously thinking about his path after football. “That really turned me onto the thought that I could make an impact in the space,” he says.

And he has. Since his NFL retirement, Kerney graduated from Columbia Business School with an MBA in 2012; spent a summer learning the ropes as an intern with an asset-management firm; created a small consulting practice, Seacon, where he focused for more than a year on teaching and presenting financial concepts to professional and amateur athletes; and in 2013 joined the NFL’s Player Engagement office, where he managed league benefits and created an annual multiday offseason NFL symposium called the Personal Finance Boot Camp that exposes players to sessions ranging from behavioral finance to multigenerational wealth preservation and is led by finance professors, wealth managers, and Kerney himself.

Wanting to take a more active, independent, and transparent role in investing client money alongside his own, Kerney transitioned in 2015 to a role as director of business development at NFC Investments, where he oversees the portfolios of a small group of clients that includes current NFL players, league veterans, and coaches. And he has leveraged all of these past experiences—as a professional, as a graduate student, as a league employee, as a registered investment adviser, and as an investor—to allow NFL players to access the unique expertise that he’s spent years accruing.

NFL teams invite Kerney to come chat with small groups of newly drafted rookies. At the Personal Finance Boot Camp, he gets up in front of a room full of veteran NFL talent as professorial PowerPoint slides flash beside him. (He also sits down one-on-one with players throughout the boot camp to comb through their specific cash flow situations as a complimentary bonus.) Like an extremely tall, very calm Suze Orman (so, maybe not like Suze Orman at all) Kerney preaches the tenets of thoughtful budgeting, the importance of concepts like compound interest and opportunity cost, the impact of taxes, and the warning signs to look for when evaluating a financial adviser or a potential investment.

“He’s big on budgeting,” says Jahleel Addae, a Los Angeles Chargers safety who along with his girlfriend and his father chose this spring to attend the NFL Personal Finance Boot Camp. “Just hearing from a guy who played the game was important,” Addae says. “Sometimes with other people, you’re like, ‘You haven’t been in my shoes.’”

As a former player who now helps counsel NFL guys on the best ways to handle their cash, Kerney’s situation seems a lot, on the surface, like that of Spencer Strasmore, the lead character played by Dwayne “The Rock” Johnson in the series Ballers, which airs on Ringer initial investor HBO. (Johnson played at the University of Miami himself.) Strasmore is a retired NFL linebacker who is forging a second career in wealth management, but the qualities that make him a lively, charismatic television presence—his disarming smile; his constant clashes with a sardonic, greedy boss; his shiny vests; his ambition and opportunism—aren’t always what define a reliable, trustworthy financial adviser in real life.

Rashard Mendenhall, the Pittsburgh Steelers’ 2008 first-round draft pick who retired from the NFL in 2014 at age 26, wrote a blog post for the Huffington Post to explain his decision, and was quickly snapped up to be part of the Ballers writing staff, bursts out laughing over the phone when asked if he’d ever trust his money to someone like Strasmore.

“I don’t know about Spencer,” Mendenhall says. “He’s a little too shaky for me. I like my money to be slow and constant. And knowing [Strasmore’s] background, and the type of athlete he was—a mad-man type of linebacker—that’s tough. But he does look good in a suit.”

“Slow and constant” would make Kerney smile. “My sales pitch is quick and simple,” Kerney says, “and doesn’t really involve tailored suits or business cards or flashy websites.”

Like Strasmore, he was an unstoppable force on the field and a fan favorite in his playing days, but that’s about where the similarities between him and the HBO character end. Strasmore is a perpetual bachelor who yacht-hops and gallivants around Miami and Las Vegas, rarely back at the office engaging in buzzkill drudgery like rebalancing portfolios or surveying spending reports. Kerney lives in Connecticut with Lisa and their four kids and recently earned a Connecticut property and casualty license, enabling him to liaise with his firm’s insurance clients in addition to the work he does as a registered investment adviser. Strasmore does indeed look good in a suit, and he knows it, peacocking around in loud custom threads; Kerney delivers presentations while wearing sensible half-zip sweaters. Strasmore’s own finances are in such shambles that he is reduced to borrowing money from his own clients; one of Kerney’s first rules of thumb is that you should never give money to anyone whose own books aren’t in transparent, impeccable order.

In one scene in Ballers’ first season, Reggie, the friendvisor to star defensive tackle Vernon Littlefield, tries to wring money out of Strasmore in exchange for getting out of his way. “You get, what, 3 percent of every dollar you handle?” Reggie asks Strasmore. “I’ll take one of those.” It’s the only episode of Ballers that Kerney has seen, and it left him queasy.

“I almost threw up in my mouth,” Kerney says. “A player agreed to give anyone 3 percent? Knowingly? For some players, they might pay 3 percent unknowingly. … I heard that, and I was like, ‘Oh my gosh, there might be some guys watching this right now saying, “Oh, I’m only paying 2 percent, not bad.”’” Kerney has the tone of a man in anguish. “Oh gosh, it’s a nightmare!” he says.

Browsing through Kerney’s Twitter feed gives one the sense that he truly does have bad dreams about NFL players who don’t #KnowTheirDough. “Too many rookies talk about working hard to make [money-bag emoji] yet won’t read a single book on how to preserve & grow it,” he pointed out in April. (#SittingDucks and #EasyTargets were the chosen hashtags on that one.) He reminds players that the NFL’s security department will perform a free background check on any prospective wealth manager to avoid situations such as Ricky Williams being allegedly conned by a woman boasting Harvard degrees that turned out not to exist. When quarterback Derek Carr signed a five-year, $125 million contract with the Oakland (and soon to be Las Vegas) Raiders in June, Kerney’s reaction was to hope that Carr had deferred a good chunk of that money to 2019 to take advantage of the difference in income tax rates between California (13.3 percent) and Nevada (0.0 percent). And he frequently comes back to a favorite refrain: It’s not what you make, it’s what you keep.

Personal finance advice often resembles weight loss tips. There is no shortage of methods and strategies out there, many preying on optimism or desperation or insecurity and promising Foolproof Secrets from the Pros. But really, the path to success in both areas is often deceptively simple: a balance sheet of calories in, calories out. In much the same way that you can spend hours on the elliptical and then promptly negate all that hard work with three margaritas, you can blow through even the biggest of big bucks quickly if you’re immediately spending on houses, or jewelry, or your friend’s brother’s new app that is definitely going to change the world, or rounds of those margaritas for all.

He’s very genuine, and a self-admitted knucklehead at times.Lester Archambeau, retired defensive end and NFLPA player director

Damaging spending can take on a number of forms, from uninterrogated financial-manager fees to soured side investments. Even players who think they aren’t making it rain can find themselves surprised by the way innocuous everyday purchases accumulate like unwanted pounds. “You go out to a nice meal once a week, and you look back, and it really adds up,” says Oakland Raiders linebacker Tyrell Adams, who scoured his budgetary habits after enrolling in the Personal Finance Boot Camp. He wasn’t the only attendee to feel this way: “I love to eat,” Addae says. “I was like, ‘Man, food is what is really taxing me!’” For Sam Young, the Miami Dolphins’ 302-pound offensive tackle, excess sustenance is a necessary cost. “As a lineman,” he says, “I guess you have to look at that as a business expense. It’s not as easy as you might think to keep on 200 pounds.”

Kerney knows that not all expenditures are silly or selfish, that many are the result of well-meaning charitable impulses. The story of a player who makes it to the pros and buys his mother a house as a thank-you for all she’s done is a common one that is often celebrated, and understandably so. But Kerney likes to remind players that they also might have a future family to take into consideration, and that if they want to put their future great-grandkids through college one day, that begins now. (Kids are freakin’ expensive, as Kerney has pointed out on Twitter.)

“I’ve had to have the come-to-Jesus conversation with people toward the end of their career,” Kerney says. “These are people with significant eight-figure net worths, who I’ll build a quick model for, and I’ll have to say: ‘Look, if you keep subsidizing Person A, and Person B, and Person C, you will have no money left to pay your own bills by the age of 46.”

And then there’s the obvious, oft-derided outlays of cash: the big, flashy, luxury purchases like watches, or mansions, or cars. Even Kerney, who drove an old Ford Bronco for much of his career before upgrading to a Honda Accord when he signed with Seattle (“Should have bought used,” he tweeted) wasn’t immune to this tendency: He sheepishly admits that when he signed his first contract with the Falcons, he complemented a piloting license he’d previously earned by acquiring a small plane. (He got rid of it when he moved to Seattle; his friends and family were no longer geographically close enough to fly the small plane for a visit, and besides, his license didn’t qualify him to operate at the altitudes needed to clear Western mountains.) There was also a time when he owned a boat, but as he told the Seattle Post-Intelligencer, he learned quickly why there’s an old joke that the two best days of a boat owner’s life are the day they buy the boat and the day they sell it; or why “BOAT” is said to stand for “Break Out Another Thousand.” On this topic, Kerney and Strasmore would fundamentally agree on the concept, if not necessarily the message: “Never buy a depreciating asset,” Strasmore explains in Season 1. “If it drives, flies, floats, or fucks, lease it!”

When Mendenhall was in the NFL, Kerney’s finance presentations had not yet begun. But the former Steeler admires the work Kerney is doing now. “It’s a great thing,” Mendenhall says. “There needs to be something to offset and counter the culture in the locker room.” (Well, unless it’s Washington’s locker room.) But Mendenhall says that he was lucky: Joe Galambos, one of his high school coaches at Niles West High School in Skokie, Illinois, taught him a lot about prudent money management. “He taught me to set things up where I wouldn’t be in a bad position when I came into the league. I knew that no matter how much I made, I wanted to set my standard of living in a way where I wasn’t spending as much as I could.” When he signed his $11 million contract with the Steelers, Mendenhall celebrated by buying himself a Jaguar—but this was in 2008, and the Jaguar he bought was a used model from 2003 that cost 20 grand.

“It’s funny,” Mendenhall says. “To this day, I still drive that same Jaguar. I would pull up to the lot and the guys would make fun of me, like, ‘You’re a first-round pick, why not buy a Range Rover?’ And really, just by not buying a $90,000 car, I kind of saved $70,000.”

Kerney says he has always had a lot of respect for the value of a dollar because he learned early what it took to earn one. As a kid growing up in Bucks County, Pennsylvania, he held a variety of summer jobs—busboy, groundskeeper at a tennis club, employee at Dairy Queen—and remembered being jealous of his four older sisters, who “all had waitress jobs and made good money.” (Kerney’s older brother Thomas, a police officer in South Carolina, died in the line of duty when Patrick was nearly 12; in 2000, Kerney established a charitable endowment in his name.)

Kerney was an excellent athlete at the Princeton Day School, where there’s now a fitness center named in his honor, and hoped to earn an athletic scholarship to college. He transferred as a sophomore to Taft, a boarding school in Connecticut, to take advantage of its outstanding ice hockey program, but realized a year in that he was overmatched in the rink, and quickly switched to wrestling. He had contemplated joining the cross-country team his first year at Taft, but “the football coach was like, ‘I think you like hitting people,’” Kerney says. “‘You can’t do that in cross-country.’” Swayed by this logic, Kerney joined the Taft football team.

But it was yet another sport, lacrosse, that earned him a scholarship to the University of Virginia. (“Pretty minimal, but more than I ever made in a summer job,” he says.) When he arrived on campus, Kerney decided he would also take a shot at trying out for the football team as a walk-on. He thought it would be more of a fantasy camp than anything else—“I thought every D-I football player was 7 feet tall with lightning coming out of their eyes”—and figured he’d be told to “go home and wait for lacrosse,” but says he didn’t want to live with the regret of not having tried. At 6-foot-5, Kerney was quite skinny—his nickname at Princeton Day School had been “beanpole”—but he nevertheless impressed the UVA football staff with his coachability and relentless pursuit of the football, and wound up playing both football and lacrosse for two years before bulking up and turning exclusively to the gridiron.

“I’m not a big endorser of aiming for your kid to be a professional athlete,” Kerney says. “The odds are stacked against you. I read an interesting article that [said] basically, when you account for all the IHL hockey players, and the Single-A baseball players, and the arena football players, it basically spat out that the median professional athlete’s income is, like, 10 grand a year.” But he wound up one of those ultra-successful outliers: At Virginia, he became an All-American defensive end, was named team captain, and eventually had his jersey number retired. The Atlanta Falcons drafted him in 1999 in the first round with the 30th pick.

Golden handcuffs is real. A lot of guys, you’re so wrapped up in this life where people expect you to be a certain person, often financially, and when the money stops coming in you lose that.Rashard Mendenhall, retired running back and Ballers writer

Lester Archambeau, a veteran who was in the second-to-last season of his career in 1999 and who was a union rep for the Falcons, recalls Kerney as “a lacrosse convert, so he was undersized—real athletic, but undersized, and he had an incredible motor.” Kerney says that one day Archambeau walked by him in the locker room and threw him a book to read. “It was The Millionaire Next Door,” Kerney says, referring to the Thomas Stanley classic of prudence and frugality. “And he said, ‘Hey, rook, if you like money, you ought to read this.’ And someone with that pedigree tossing me a book? You read the book.” He now considers it a must-read, along with Warren Buffett’s biography and John Bogle’s The Little Book of Common Sense Investing.

Archambeau, who is now a player director in the NFLPA, isn’t certain how he came across the Stanley book himself. “Maybe it was NPR,” he says. “I was listening to a lot of Paul Harvey at the time. Maybe he pushed it.” As for his role in helping plant the seeds for Kerney’s second career when the rookie was barely beginning his first one, Archambeau admits: “I had no idea [the book] was going to make such an impact on him. It was a cool experience, after the fact, to have him come back and share that with me.”

Kerney spends a lot of time thinking about the most effective ways to get his message through to a group of players with whom he might spend only an hour. He appeals to the things he knows to be true about their competitive personalities, warning them that the same sense of nobody-believed-in-me bluster that helped get them to where they are can backfire if it means they are too stubborn or proud to ask lots of questions. He likens being a professional athlete to winning a lottery ticket—and reminds players that, having already hit the jackpot, they don’t necessarily need to seek out additional risky prospects, like one-off real estate deals or tech investments, until they’ve established a solid, safe asset-growth base first.

Kerney is particularly passionate about the impact of hidden fees or management costs on a player’s portfolio, because, given the young age of the athletes, even amounts that seem relatively insignificant now will, over time, go forth and multiply. The way Kerney sees it, every dollar spent by a player today—on lavish vacations, on mutual fund fees, on cufflinks, on The Next Facebook—is a dollar that could have been stashed in the stock market. Assuming a growth rate of 7.5 percent, which he considers to be a conservative proxy for long-term stock market returns based on historical averages, a dollar today grows into $77 over a player’s remaining lifespan of, say, 60 years.

“So I say, ‘Guys, if you want to spend an extra $100,000 this year, that is your choice,’” he says. “‘But understand that you are spending about $7.7 million.’ That always pops some eyeballs around the room, especially for someone who may have just spent a hundred thousand on their watch.”

My sales pitch is quick and simple, and doesn’t really involve tailored suits or business cards or flashy websites.Patrick Kerney

“What I thought was cool about a presentation he gave,” Archambeau says of a visit Kerney made to an NFLPA event for rookies, “is that he’s very genuine, and a self-admitted knucklehead at times. But one thing he said was that, much like his football career, he came in not knowing a lot and dedicated himself to becoming a better player every day, every year. As a rookie, he struggled, like all the rookies do. But his spiel was like, ‘It’s the same thing with your finances. You guys know nothing, and there’s nothing wrong with that; that’s fine. Make yourself learn something every year.’ I thought that was really smart, equating it with how all our guys work on their craft as a player.”

Ultimately, Kerney’s goal for the NFL players he works with is financial security—which translates into personal freedom. This is a concept with which Mendenhall, in particular, can very much relate. When he decided to retire in his mid-20s, it wasn’t because of debilitating injury or anything like that. It was because, while he’d enjoyed his days as a football player, he had long felt that there were other things he wanted to do more. “When I was playing football, I was always writing,” Mendenhall says. “Writing was something I always did, even back in college and high school.”

That Mendenhall now has a professional TV-writing gig is part serendipity, part his own doing. Had he retired a year earlier, or a year later—had he not written a blog post for HuffPo that blew up—he probably wouldn’t have been in the right place at the right time for Ballers to call. But had he not been conservative about his spending when he was in the league, he might not have been in a position to select his retirement date in such a manner. “Golden handcuffs is real,” he says. “A lot of guys, you’re so wrapped up in this life where people expect you to be a certain person, often financially, and when the money stops coming in you lose that. So guys keep playing—they’re like, ‘Another year, another contract, I’ll be safe.’ It swallows you to where your heart’s not in it, where even if you need to do something else, the pressure to keep playing is too great.”

Stories of bankruptcy and fraud and implosion are what often dominate headlines—the stuff of Ballers drama, indeed. “You hear all these horror stories about athletes mismanaging their money,” says Jamize Olawale of the Oakland Raiders, who attended the Personal Finance Boot Camp in 2016 with his wife. “You just never know who has your best interests in mind.” What you don’t hear much about are the players like Mendenhall, who have early influencers in their lives who give them beneficial, lasting advice; or the various players who, Kerney says, enjoy positive outcomes from their conservative, plain-vanilla investment decisions. “They’ve been boringly slogging along in public securities, by doing a high percentage of their stuff in indexes,” he says. “It doesn’t make for a story.”

To #KnowYourDough means to keep learning, to ask questions without fretting about sounding vulnerable or dumb, to be a pest, to think about the future generations of your family and the passions you want to pursue, to be wary of the Spencer Strasmores of the world, to be OK with boring. “And another thing [Kerney] says,” Addae says, “is when you’re dealing with a financial adviser, you want to make sure that if they tell you to put their money somewhere, you make sure that’s where they’re putting their money, and their kid’s money.” In other words: It’s time to start saving up for some serious gumballs.