This story was updated on February 8, 2017.

Like any good Kardashian-adjacent reality star, Blac Chyna operates a bustling side business promoting waist trainers, tooth whiteners, and other lifestyle flotsam on Instagram. She’s currently on a promo spree for Lyft, just like Rob Kardashian. But Chyna’s account has a sponsored-content habit that deviates from the laxative-tea-themed playbook. Sandwiched between glam ass shots and videos of her children, Chyna has advertised something called “Obama’s student loan forgiveness” plan to her more than 11 million followers.

If Chyna aficionados were spurred to action by her urgent-sounding financial advice, they were surely disappointed, because “Obama’s student loan forgiveness plan” does not exist.

“My whole body just cringed when you said that,” Betsy Mayotte, the director of consumer outreach and compliance at Boston-based nonprofit American Student Assistance, said when I asked if she was familiar with “Obama’s student loan forgiveness plan.” Mayotte is deeply familiar. She counsels people who have college finance problems, and she often deals with the aftermath of what happens when they’ve been taken in by the magical-sounding words that “student debt relief” companies use in their advertisements for fake plans. These companies warn students to sign up for their services or lose their chance at a debt-free youth, with outlandish promises like “$17,500 in Up Front Forgiveness?” and “GET RID OF YOUR DEBT TODAY!”

These companies are vultures circling people who have been wounded by the student loan industry, which is pocked with corruption and negligence. For-profit colleges, like the University of Phoenix and the now-defunct Corinthian Colleges, have helped create a full-fledged debt crisis. These for-profit colleges encourage students, many of whom lack financial resources and experience, to take out large loans to finance their expensive educations, and do so by frequently exaggerating the chances of job placement after graduation. The U.S. Department of Education has forgiven some student debt from Corinthian Colleges, which closed its campuses in 2015. And predatory universities are only one part of the problem. The third-party companies that manage student loans are an even more scurrilous element of the crisis. No matter where people go to school, once they receive student loans, the companies that help manage those loans often fail to help them pay off their debt effectively. This is why the Consumer Financial Protection Bureau is suing major student loan lender Navient (formerly part of Sallie Mae), accusing it of “failing borrowers at every stage of repayment.” Two of the infractions alleged in the complaint are that Navient would incorrectly report that disabled veterans had defaulted on their loans, which hurt their credit, and that it would steer its clients into repayment programs that were not in their best interest. [Update: After this story was published, Navient sent The Ringer its statement about the lawsuit, calling the allegations false and politically motivated, and saying that it will defend itself in court.]

When schools use misleading advertising to entice people to take out loans they can’t afford and servicers like Navient fail to help people pay, it helps grow a vulnerable population. In 2015, one in six people with student loans from the federal government were in default, according to The Wall Street Journal. That’s around 3.6 million people desperate for a solution to mounting debt. These are the people targeted by brazen “Obama student loan forgiveness” crews.

These kinds of ads use generic, benevolent-sounding names like College Education Services and Student Aid Institute to sound legitimate, but in reality they are often ramshackle operations designed to disappear when they’re scrutinized. Several debt experts I spoke with characterized them as “fly-by-night.” The phrase “whack-a-mole” was also used repeatedly, since many of the companies are small operations that simply declare bankruptcy, change their names, and start over when complaints roll in, making them difficult to catch and permanently stop. It’s stand-out villainy in an industry rife with bad guys.

There are a few different models of the “Obama’s student loan forgiveness” ploy and other too-good-to-be-true gambits. Some of these companies convince students to pay them to act as superfluous middlemen, and charge steep payments to do what any student can do for free. In those cases, the companies do technically provide a document-processing service, but their service is an unnecessary one, since they charge money to “process paperwork” that people can fill out for free online. Meanwhile, other companies demand upfront or monthly payments in exchange for help in lowering interest rates. But all they do is place loans into temporary forbearance, which means loans are postponed and students don’t have to pay for a set time period. This creates the illusion that the company has made things easier, but in reality, they have only delayed payments for a few months.

“The worst scams are the ones where people are paying a large upfront fee and nothing happens to their student loans,” said student loan expert Robert Farrington, who runs a website called The College Investor. “In pretty much every scenario … the student loan borrower is out of money. The worst I’ve seen is upward of $2,500 to $3,000.” Other companies just take the money and disappear. These companies act illegally in a variety of ways, including “charging illegal advance fees before providing any services, deceiving customers about the costs of their services, falsely promising lower monthly payments, falsely claiming quick relief from default or garnishment, and falsely representing an affiliation with the U.S. Department of Education,” a Consumer Financial Protection Bureau spokesperson told The Ringer.

In all cases, the companies obscure the fact that they exist purely to profit. They take advantage of confusing federal loan repayment and consolidation plans, and how little companies like Navient (whose lawsuit is ongoing) do to help people in need. As a loan servicer for the federal government, Navient was required to help people learn about and sign up for alternative repayment plans, including one tailored for people with low incomes. But the Consumer Financial Protection Bureau’s complaint alleges that Navient “systematically deterred” borrowers from signing up for the right plan, and steered them into plans that hurt them financially.

The lures are so effective because they’re laced with just enough truth to seem possible. Student loans can be painfully real and routinely are daunting. The “Obama” hook seems believable because the Obama administration did introduce a variety of programs meant to alleviate the burden of student loans, including repayment plans based on income. (And perhaps President Obama’s emphasis on hope left a subliminal impact of sorts.) But “Obama’s student loan forgiveness plan” wasn’t concocted in the White House. It’s a hustler’s invention, a bogus catchphrase designed to raise hopes.

Student loan forgiveness scams have taken off only in recent years, but they have a connection to another type of Great Recession–era swindle: the mortgage forgiveness scam. When the CFPB shut down a swindle called Student Aid Institute Inc. in March 2016, Director Richard Cordray noted the parallels between the two types of con. “We see more and more companies and websites demanding large upfront fees to help student loan borrowers enroll in income-driven plans that are available for free,” Cordray said in a statement. “These practices bear a disturbing resemblance to the mortgage crisis where distressed consumers were preyed upon with false promises of relief. We will continue to shut down illegal scams and address sloppy servicing practices that victimize consumers,” he said, referring to a rash of rip-offs targeting people affected by the mortgage crisis in the late 2000s.

The U.S. Department of Education warned students against these companies last year, in a blog post titled “Don’t Be Fooled: You Never Have to Pay for Student Loan Help” and with a YouTube video starring John King, then the acting education secretary.

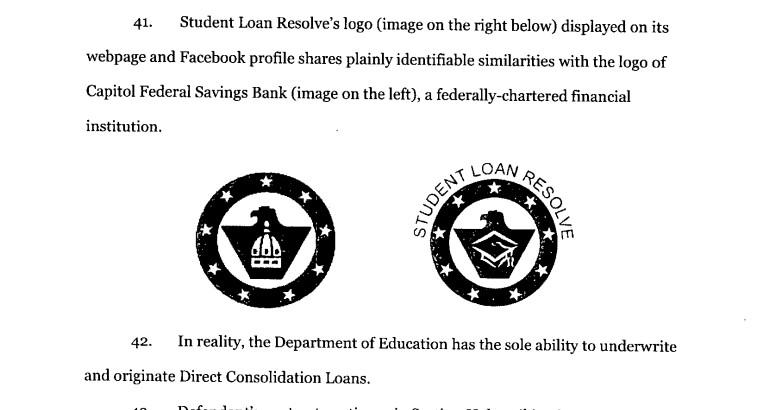

Illinois Attorney General Lisa Madigan has taken an aggressive approach to penalizing these companies, and the lawsuits her office has filed provide a window into this industry. One suit, against a company operating as Student Loan Resolve, includes illustrations that the AG says show how the company hijacked the logo of a legitimate organization to give off the impression of professionalism.

According to the lawsuit, Student Loan Resolve falls into the first category of student loan scams: It does process student loan documents, so it doesn’t just take money and disappear. But as the lawsuit points out, the Department of Education’s guidance states that student borrowers are not permitted to give anyone their personal identification number to log in and change payment options. Yet Student Loan Resolve required customers to give up their PINs. It framed its service as a route to great repayment options, with claims like, “We have Forgiveness Programs to help people who are in eligible professions.” (Emphasis from the Illinois AG.)

The lawsuit, filed in 2015, claims that Student Loan Resolve violates two Illinois consumer protection laws. Despite the lawsuit, Student Loan Resolve is still operating; the company tells students that it will continue to help them process their federal student loans.

Stealing legitimate businesses’ logos appears to be a trend with these companies. “[A company] stole our old logo,” said Natalia Abrams, the cofounder and executive director of StudentDebtCrisis.org. “And [they] were using it to try to convince students that they were a reputable company, and we had to send them a cease-and-desist.”

Abrams works as an advocate for people with student loans, so there is a grim irony in the way her organization’s logo was co-opted by the exact kind of behavior she fights. “That’s when we realized who they were, and how low they would go, frankly, to try to convince student loan borrowers that they were a safe company,” she said. “We’ve only seen them get more sophisticated over time.

“They sell themselves as private consolidation companies, but nowadays we’re seeing them go school specific,” Abrams continued. “I attended UCLA, and I’ll see, ‘UCLA students, there’s a special deal from your school,’ and it looks like it’s actually coming from UCLA and in fact it’s a private debt-relief company that has nothing to do with your school.”

Abrams’s StudentDebtCrisis.org teamed up with NerdWallet to conduct a survey on student-debt-relief scams in July 2016. Responders painted a bleak picture:

“I realized it was fraud and called to cancel,” said Joni Geary, a respondent from Michigan. “However, they still took $200 from me and wouldn’t return it, stating that there was no refund even when I never signed their contract.”

Attorneys general across the country have issued warnings and pursued lawsuits against these companies. Meanwhile, the Federal Trade Commission is paying attention. It partnered with Florida’s attorney general to crack down on two student debt relief companies in the spring of 2016. And yet the debt-relief scams show no signs of slowing down. In April-June 2016, complaints to the CFPB regarding student loan companies increased 62 percent over the same period the year before — more than any other type of loan complaint. (For comparison, mortgage complaints decreased 2 percent, while complaints about payday loans dropped by 15 percent.)

This is digital skulduggery on the rise.

I first found out about this unscrupulous business after reading about Blac Chyna’s foray into it. I contacted Chyna’s team to ask how she got tangled up in the industry, but received no response. “We don’t get a lot of celebrity endorsements in the student loan industry,” Mayotte told me. “Blac Chyna and the student loan industry is just such a bizarre little connection.”

Mike Heller, the CEO of Talent Resources, which arranges sponsored content on celebrity accounts, works with Chyna’s representation, but did not work on the debt-relief post. He emphasized that his company requires vetting before partnering a brand with a company. “We really protect the brand and make sure that they know everything they’re getting into, because you’re talking about Blac Chyna,” he said. “That’s someone that might’ve just done [the deal] directly with her team but didn’t protect the brand.”

While celebrity social media endorsements are rare, advertising online for this type of scheme is common. Many of the fly-by-night companies began advertising online through web ads on search engines like Google and Yahoo, Farrington said. The companies would play the search engine optimization game so that their web pages would appear first when people typed in terms like “student loan forgiveness.” The problem became so prevalent that the CFPB sent a letter to the search engines asking them to crack down on fraudulent and misleading companies.

In 2015, researcher Sam Adler-Bell looked into how student debt relief companies advertise, and he found that searching for “student debt relief” on Google pulled up third-party companies rather than official government sites, which were included in the search results, but below the third-party options. In particular, a company at the URL www.studentdebtrelief.us showed up very high in search results. Despite its official-looking name, www.studentdebtrelief.us is not a government-affiliated website. Two years later, in 2017, a Google search for “student debt relief” continues to pull up this URL. (Adler-Bell noted that Student Debt Relief was in a “regulatory grey zone” because while it did charge a processing fee to send in loan forms that someone could fill out themselves, it didn’t appear to demand money upfront.)

Still, Farrington believes that search engine crackdowns have made enough of a difference to cause a change in behavior. “Since then, it’s been much more difficult for them to pay for advertising on search engine platforms, so they’ve migrated toward social media platforms,” Farrington said. Instagram advertisements are a more recent twist on the concept, and have popped up only in the past six months or so, according to Farrington.

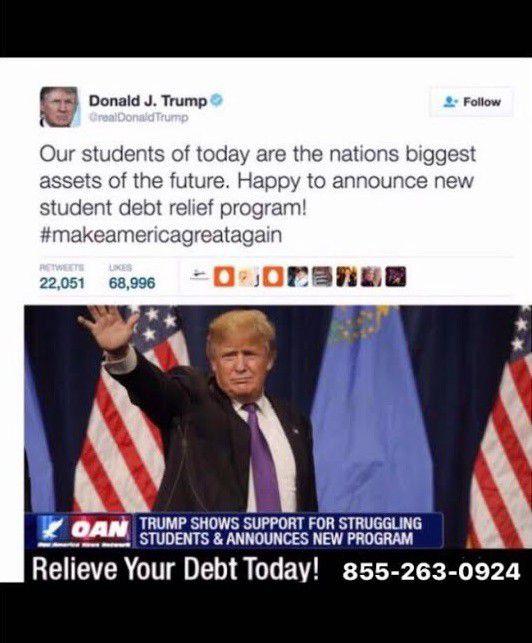

Right now, anyone can find ads for “Obama student loan forgiveness” on Instagram by doing keyword searches like “#studentloans.” And these scams are evolving with the times — the CFPB sent along a screenshot of a Trump-specific version of the ad:

The story of Nichelle Culver illustrates just how sketchy these ads can be. As WCPO Cincinnati reported in 2016, Culver — saddled with student loans — was “captivated by a Facebook ad that said ‘billions in student loan debt has been forgiven.’” Culver said that she called the number on the Facebook ad because it promised that Obama was giving away student loan money, and she assumed it was a federal program. The person on the other end, however, told her she needed to purchase a $300 iTunes gift card as her application fee. After she did that, the company asked for even more money. “They would need an additional $500. I was like $500? I just gave you $300, I’m not going to give any more,” she told WCPO. She didn’t give them more, but she was left $300 poorer, with nothing to show toward loan relief.

Natalia Abrams says that ads for these companies are common on Facebook. “I feel if Facebook is going to have a warning for fake news, they should have a warning for fake loan companies,” she said.

These student debt relief companies capitalize on confusion, so I want to be as clear as possible: For people with private loans — from a bank, for example — there can be a benefit in talking to a third party about how to consolidate. Not all companies providing financial services to people with student loans are slimy. There are third-party companies offering legitimate, helpful service, and having con-lovin’ doppelgängers is the bane of their existence. Max Spiegel, the COO of Student Loan Hero, which offers financial advice to people with student loans, says some clients show up after being scammed elsewhere. “Refinancing isn’t for everybody. Any company that tries to send you directly to a refinance is really — without telling you what the considerations are, so to speak — doing you a disservice,” he said.

But many student loan borrowers don’t ever need to work with a third party.

“If you have federal loans, you do not need to pay for basic student loan help, you do not need to pay for consolidation, you do not need to pay to get into the income-driven repayment programs, and you do not need to pay for public-service loans forgiveness or default rehab,” Abrams said. “There are times you might need an attorney or a specialized credit counselor, but those are so rare that it’s pretty safe to say that you do not need to pay for student loan help.” Abrams noted that private loans are a different story.

So, what to do? I talked to Gregory Fitzgerald, a California-based lawyer who often works with people in debt. Fitzgerald’s clients have dealt with out-and-out student loan scams, where someone has paid a company money to help manage their loans and seen nothing in return, as well as situations where someone paid companies to consolidate loans that they could’ve easily consolidated for free. I asked Fitzgerald what sort of legal recourse scam victims can take. He recommends contacting the CFPB to try to shut the company down. “I see this as an unauthorized practice of law. I mean, these are complex contracts, these student loans and the repayment plans and the federal loans and the Department of Education. These are not simple things to understand,” Fitzgerald said. “I wish the state bars would be more active, because I think these guys are sort of selling illegal services.”

But chasing down money is difficult, as many cash-strapped clients lack the funds to go after their scammers. It’s often not worth it to hire a lawyer to chase these companies, especially when so many of them tend to abruptly disappear when they feel heat.

The biggest bulwark that students have against getting ripped off is getting educated. The more people who know they don’t need to pay to get federal student loan repayment options, the less effective these scams will be. Unfortunately, because so many people are financially bound by heavy loans, these companies offer hope for relief that simply doesn’t exist. This rotten cottage industry popped up because the official student loan industry gave it every opportunity to do so. Legitimate-seeming, enormous businesses like Navient are accused of failing on such a profound level that they made people desperate enough to believe improbable promises on shady-looking Instagram ads from reality stars.